Traditional economic theory posits that individuals make rational, well-informed decisions. However, we know this to be an oversimplification. Several psychological investment pitfalls can derail even the most seasoned investors.

By becoming aware of and actively working against our innate behavioural biases, investors can reach more impartial decisions. Enter the field of behavioural finance, which sheds light on investor psychology and the true motivations behind financial behaviour.

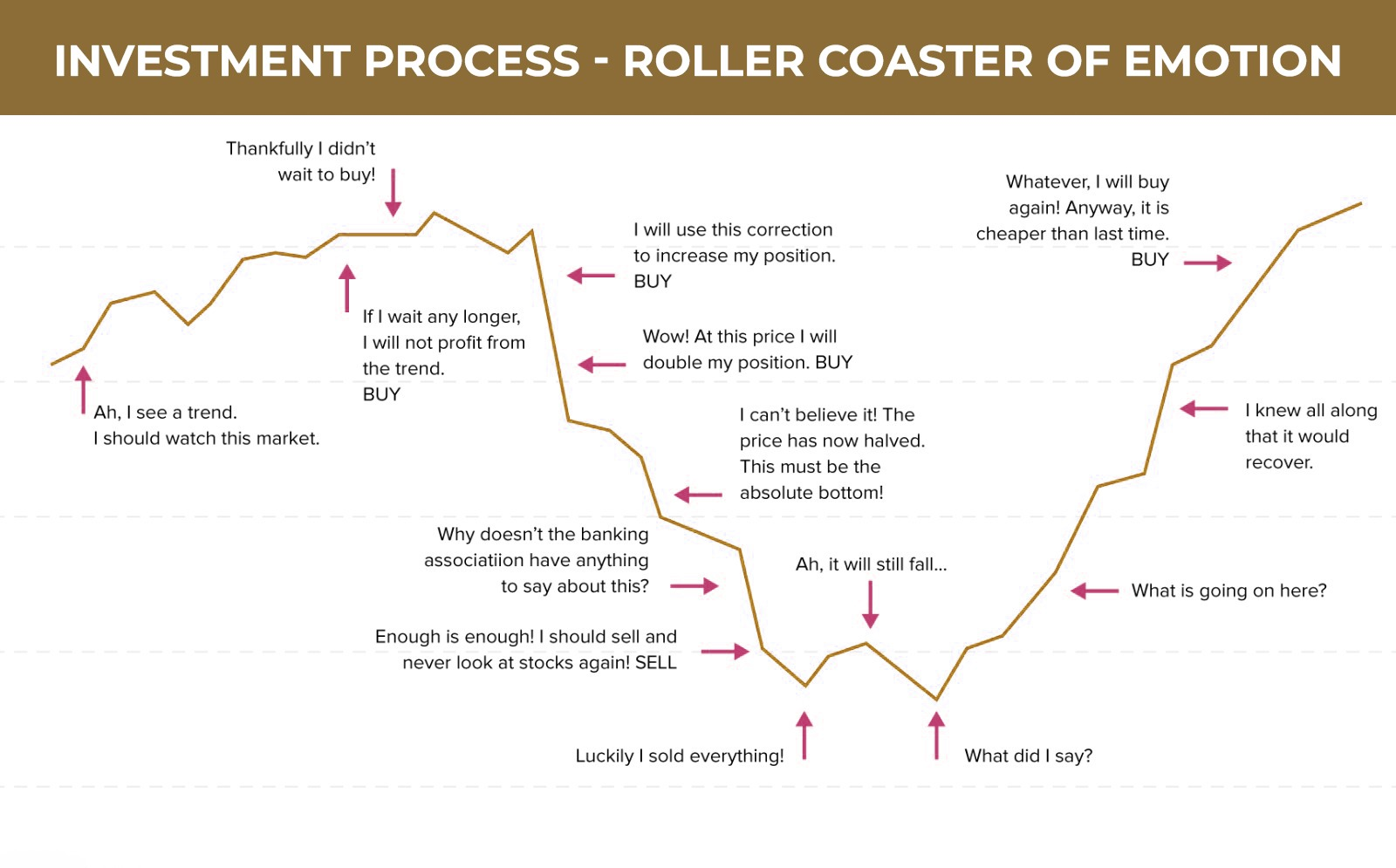

The Roller Coaster of Emotions

Investors often experience an emotional rollercoaster during the investment process. This cycle involves information gathering, stock selection, holding and selling investments, and finally, making new selections.

Source: Credit Suisse

Unfortunately, this cyclical process is fraught with psychological traps. To make clear-headed decisions, investors need to recognise and combat common behavioural biases.

Traditional vs. Behavioural Finance

Established economic and financial theories assume individuals are consistently rational in their decision-making. This framework implies two things:

- Investors correctly update their beliefs when they receive new information, and

- They make normatively acceptable choices.

While appealing in its simplicity, this view fails to reflect human reality. Humans often act irrationally, in systematic and counterproductive patterns. Studies reveal that 80% of individual investors and 30% of institutional investors fall prey to inertia rather than logic.

These deviations from theoretical predictions have paved the way for Behavioural Finance, essentially the psychology of investing. This field draws on psychology, sociology, and even biology to investigate true financial behaviour.

Behavioural Biases and Their Impact on Investment Decisions

Deeply ingrained biases lurk within our psyches. While often helpful in everyday life, they can sabotage our efforts when it comes to investing.

Behavioural biases encompass both cognitive and emotional biases.

- Cognitive biases stem from errors in our thinking, such as statistical, information processing, or memory shortcomings.

- Emotional biases, on the other hand, arise from feelings rather than facts, causing us to act on impulse or intuition.

Let’s delve into the most common behavioural biases that lead to investment pitfalls:

1. Overconfidence

Humans generally have a positive outlook. For example, a 1980 study revealed that a staggering 70-80% of drivers considered themselves above-average behind the wheel. Similar overconfidence manifests itself in other professions, including doctors, lawyers, and CEOs. Though confidence can be an asset, excess confidence can cloud our investment decisions.

Overconfidence is an emotional bias, leading investors to believe they have more control over their investments than they actually do. As investing involves complex forecasts of an unknowable future, overconfident investors often overestimate their ability to identify winning stocks. In extreme cases, overconfidence can even make investors susceptible to financial fraud.

2. Self-Attribution Bias

Self-attribution bias occurs when investors credit successes to their own actions while blaming external factors for failures. This bias is a form of self-protection or self-enhancement. Under its influence, investors may become overconfident, leading to underperformance. To combat this, track your mistakes and successes, and develop systems to hold yourself accountable.

3. Active Trading

Studies consistently demonstrate that excessive trading (active trading) leads to market underperformance. Investors utilising traditional brokers often fared better than online traders who trade more frequently and speculatively. This underperformance is often attributed to investor overconfidence.

4. Loss Aversion

The established financial theory holds that risk and return have a direct relationship – the higher the risk, the higher the potential reward. This assumes investors seek the highest return possible based on their risk tolerance. However, behavioural finance research throws this into question.

5. Fear of Loss

Pioneers of Behavioural Finance, Dan Kahneman and Amos Taversky, conducted a seminal study on how people view risk and reward. They proved that investors are more sensitive to loss than to potential gain.

In short, we hate losing more than we love winning. This means we’d rather choose not to lose £10 than have a chance of potentially finding £10.

Some estimate that people weigh losses more than twice as heavily as gains. Fear of loss, however small, can lead to costly decisions like taking smaller, sure losses instead of risking the possibility of a larger expense.

6. Disposition Effect

Due to loss aversion, investors frequently hesitate to realise losses, holding onto losing stocks in the hope of a recovery. This “disposition effect” describes investors’ tendency to sell winning positions prematurely but cling stubbornly to losing ones.

This effect can significantly increase investors’ capital gains taxes, as regulations often incentivize deferring gains as long as possible.

How do Behavioural Biases impact Portfolio Construction and Diversification?

Modern portfolio theory, formulated by Nobel Prize-winning economist Harry Markowitz, states that individual securities should not be evaluated on their own, but rather by how they contribute to the portfolio’s overall profile.

In practice, however, investors tend to become hyper-focused on specific investments, leading to a “narrow frame” that heightens loss sensitivity. By adopting a “wide frame” to assess performance, investors are more prepared to accept short-term losses.

We tend to mentally compartmentalise expenses or investments into categories like “school fees” or “retirement”. These buckets often hold different risk tolerances. However, mental accounting can violate economic principles.

For instance, an unexpected windfall designated as “fun money” might be spent more frivolously than a salary increase with the same value. Investors tend to lose sight of their overall wealth position and focus too heavily on individual buckets.

Moreover, despite the benefits of diversification, investors often favour familiar investments – those from their own country, region, or company. This familiarity bias can also manifest as an extreme preference for investing in one’s own employer’s stock. This is a dangerous gamble for employees, as a downturn in the company’s fortunes can result in both job losses and erosion of retirement savings.

Some Behavioural Biases are Based on Misinformation

Some biases stem from misinformation. These include:

- Anchoring: Investors tend to cling to an initial belief and use it as a mental anchor point for future judgments. We often base decisions on an initial piece of arbitrary information (like a stock’s purchase price). Consequently, this makes it difficult to adjust our views when presented with new information.

- Representativeness Bias: This bias leads investors to hastily label an investment as good or bad based solely on its recent performance. They might buy stocks after price rises, wrongly assuming a winning streak will continue, and ignore stocks that seem to be trending downwards.

- Gambler’s Fallacy: Related to representativeness bias, the gambler’s fallacy refers to the tendency to see patterns where none exist. Investors often try to impose order on inherently random processes.

- Attention Bias: Traditional financial theory treats buying and selling as two sides of the same coin. In reality, investors are more likely to buy stocks that catch their attention – those in the news, exhibiting unusual trading volume, or with extreme one-day returns. The problem arises when the attention-grabbing quality actually detracts from the investment’s potential.

Cultural Influences on Investing

Alt: Cultural influences on Investing

Traditionally, economists assumed biases were universal. But there’s an emerging field – Cultural Finance – which is proving this wrong. It examines how factors such as society and culture shape financial decision-making. Both behavioural finance and cultural finance illuminate deviations from the traditional rationality model.

Dutch sociologist Geert Hofstede offers one of the most influential definitions of ‘culture’. He describes it as ‘collective mental programming’ manifested in values, norms, rituals, and symbols. Cultures emphasise different aspects of this ‘programming’ to varying degrees. Let’s examine how cultural dimensions influence investing tendencies:

International Differences in Loss Aversion

Researchers analysed the time preferences, risk attitudes, and behavioural biases of almost 7,000 investors in over 50 countries. Even after controlling for national wealth, they found stark differences in loss tolerance. Anglo-Saxon countries exhibited the highest tolerance for loss, while Eastern European investors displayed the greatest aversion.

Key cultural dimensions linked to loss aversion include individualism, power distance, and masculinity.

Individualistic cultures, like those in the West, place importance on personal values and achievements. This fosters a strong emotional attachment to possessions, including investments. In contrast, collectivist societies, often found in East Asia, emphasise interdependence and group harmony. This holistic perspective makes it easier for individuals to cope with losses, and the presence of strong social support networks further softens the blow.

The Power Distance Index (PDI) measures how power and wealth are distributed within a society. A culture with a high PDI often has a rigid hierarchy, discouraging assertiveness and emotional expression. This inequality can fuel feelings of helplessness and pessimism when it comes to the consequences of loss, leading to heightened loss aversion.

International Differences in Temporal Preferences

The same study explored time preferences across cultures. Investors from Nordic and German-speaking countries demonstrated the greatest patience, while African investors were the least patient. Cultures with Germanic/Nordic, Anglo/American, Asian (66-68%), and Middle Eastern origins displayed a higher willingness to wait for future gains.

Two cultural dimensions affect time preferences: Uncertainty Avoidance (UAI) and Long-Term Orientation (LTO). Societies with high UAI are less tolerant of ambiguity and the unpredictable nature of the future. Consequently, they tend to favour immediate rewards over those in the distant future.

Societies with high LTO, such as those in East Asia, place great value on the future and exhibit greater investment patience. It’s worth noting that dominant religions in Southeast Asia, like Hinduism and Buddhism, emphasise the concept of “rebirth,” framing our current life as a small part of a much grander timeline.

How Cultural Differences Impact the Portfolio Management?

Interestingly, research shows that individualism, masculinity, and uncertainty avoidance strongly influence cross-border investment decisions. Individualism and masculinity encourage foreign diversification, while uncertainty avoidance is associated with the “home bias” – investors remain heavily concentrated in familiar investments.

Home bias weakens with increased investor sophistication!

Similarly, when it comes to asset management, in uncertainty-avoidant countries, managers frequently avoid deviations from their portfolios’ benchmark indices, instead channelling energy into intensive research to mitigate risk. While managers in the U.S., the culture with the lowest uncertainty avoidance, spend less time on explicit research.

Behavioural Finance is an Evolving Field

While we can’t eradicate hardwired behavioural biases, awareness is the first step towards mitigating their negative effects. By employing systems designed to counter these instincts – utilising feedback trails, decision audit trails, and checklists – we can improve decision-making and significantly boost our chances of investment success.

If you are a B.Com or an M.Com student and aspire to become an individual investor, investment manager, financial planner, or broker, understanding the psychological forces behind financial decisions is paramount to your enduring success. Behavioural finance and niche fields like Cultural Finance and Neuroeconomics are easier to break through and can catapult you to success.

Arm yourself with the knowledge of behavioural finance to protect yourself and your organisation from common investment pitfalls and take charge of your financial future.